EDUCATION CREDITS AREN’T JUST FOR CHILDREN’S TUITION

On December 22, 2017, The Tax Cuts and Jobs Act was signed into law. The information in this article predates the tax reform legislation and may not apply to tax returns starting in the 2018 tax year. You may wish to speak to your tax advisor about the latest tax law. This publication is provided for your convenience and does not constitute legal advice. This publication is protected by copyright.

Article Highlights:

- Who Qualifies for Education Credits

- American Opportunity Credit

- Lifetime Learning Credit

- Qualifications

- Who Gets the Credit

If you think that education credits are just for sending your children to college, think again; the credits are available to you, your spouse (if you are married), and your dependents. Even if you or your spouse is only attending school part time, you still may qualify for a tax credit.

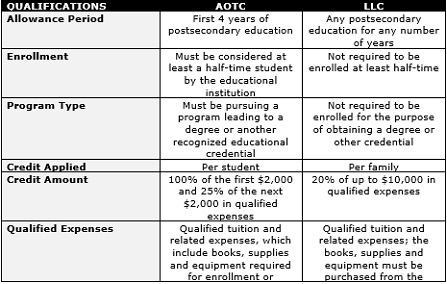

There are two education-related credits available: the American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC). For either credit, the student must be enrolled in an eligible educational institution for at least one academic period (semester, trimester or quarter) during the year. An eligible educational institution is any accredited public, nonprofit, or proprietary postsecondary institution that can participate in the U.S. Department of Education’s student aid programs.

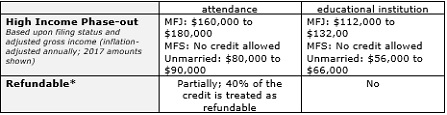

The credits phase out for higher-income taxpayers who are married filing jointly (MFJ) or who are unmarried. Those who are married filing separately (MFS) do not qualify for either credit.

The following table provides the qualifications for both credits:

*Generally, credits are nonrefundable, meaning that they can only be used to offset your tax liability; any amount exceeding your current-year tax liability is lost. However, unlike other credits, the AOTC is partially refundable in most cases.

Many individuals who both work and attend school can be enrolled less than halftime and still qualify for the LLC.

Another interesting twist to education credits is that the taxpayer who qualifies for and claims the student’s exemption for the year gets the credit—even if someone else pays the expenses. Thus, for example, even if a noncustodial parent pays a child’s college expenses, the custodial parent gets the credit if he or she is otherwise qualified. The same applies when grandparents help pay for their grandchild’s education; the grandparents do not qualify for the credit unless they, and not the child’s parents, claim the student as a dependent.

Generally, the educational institution sends a Form 1098-T to the taxpayer (or dependent); this includes the information necessary to complete the IRS form and claim the credit. Unless the IRS has exempted the educational institution from having to file a 1098-T, the law requires the taxpayer to have this 1098-T in hand to claim either of the credits.

If you have questions about how this these education tax credit provisions apply to you, please give this office a call.

Leave a Reply

Want to join the discussion?Feel free to contribute!